Questions & Answers about…

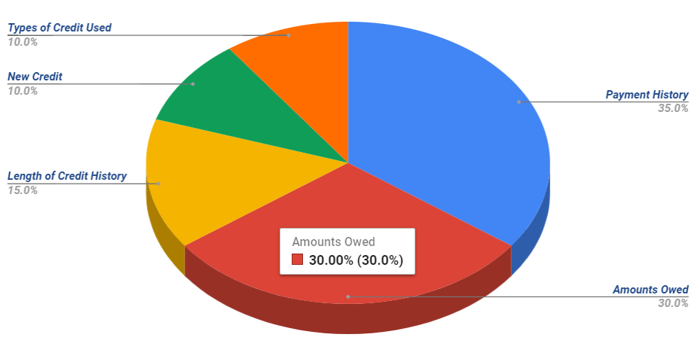

Payment History

- Account payment information on specific types of accounts (credit cards, retail accounts, installment loans, finance company accounts, mortgage, etc.)

- Presence of adverse public records (bankruptcy, judgments, suits, liens, wage attachments, etc.), collection items, and/or delinquency (past due items)

- Severity of delinquency (how long past due)

- Amount past due on delinquent accounts or collection items

- Time since (recency of) past due items (delinquency), adverse public records (if any), or collection items (if any)

- Number of past due items on file

- Number of accounts paid as agreed

Amounts Owed

- Amount owing on accounts

- Amount owing on specific types of accounts

- Lack of a specific type of balance, in some cases

- Number of accounts with balances

- Proportion of credit lines used (proportion of balances to total credit limits on certain types of revolving accounts)

- Proportion of installment loan amounts still owing (proportion of balance to original loan amount on certain types of installment loans)

Length of Credit History

- Time since accounts opened or since account activity

- Time since accounts opened, by specific type of account

New Credit

- Number of recently opened accounts, and proportion of accounts that are recently opened, by type of account

- Number of recent credit inquiries

- Time since recent account opening(s), by type of account

- Time since credit inquiry(s)

- Re-establishment of positive credit history following past payment problems

Types of Credit Used

- Number of (presence, prevalence, and recent information on) various types of accounts (credit cards, retail accounts, installment loans, mortgage, consumer finance accounts, etc.)

- Your race, color, religion, national origin, sex and marital status - US law prohibits credit scoring from considering these facts, as well as any receipt of public assistance, or the exercise of any consumer right under the Consumer Credit Protection Act.

- Your age - Some scores may consider your age. FICO scores do not.

- Your salary, occupation, title, employer, date employed or employment history

- Where you live - Lenders may consider this information; however, this type of information is generally not available in the credit file to be used for the calculation of a score.

- An interest rate being charged on a particular credit card or other account

- Items reported as child/family support obligations or rental agreements

- Certain types of inquiries or requests for your credit report - The score does not count "consumer-initiated" inquiries — requests you have made for your credit report, in order for you to check it. It also does not count "promotional inquiries" — requests made by lenders in order to make you a "pre-approved" credit offer — or "administrative inquiries" — requests made by lenders to review your account with them. Requests that are marked as coming from employers are not counted either.

- Any information not found in your credit report

- Any information that is not proven to be predictive of future credit performance

- Whether or not you are participating in credit counseling of any kind

- A score takes into consideration all these categories of information, not just one or two. No one piece of information or factor alone will determine your score.

-

The importance of any factor depends on the overall information in

your credit report.

For some people, a given factor may be more important than for someone else with a different credit history. In addition, as the information in your credit report changes, so does the importance of any factor in determining your score. Thus, it is impossible to say exactly how important any single factor is in determining your score — even the levels of importance shown here are for the general population, and will be different for different credit profiles. What is important is the mix of information, which varies from person to person, and for any one person over time.

-

Your credit score only looks at information in your credit report.

However, lenders look at many things when making a credit decision including your income, how long you have worked at your present job and the kind of credit you are requesting.

- Your score considers both positive and negative information in your credit report. Late payments will lower your score, but establishing or re-establishing a good track record of making payments on time will raise your score.

Facts & Fallacies

Fallacy: My score determines whether or not I get credit.

Fact: Lenders use a number of facts to make credit decisions, including your credit score. Lenders look at information such as the amount of debt you can reasonably handle given your income, your employment history, and your credit history. Based on their perception of this information, as well as their specific underwriting policies, lenders may extend credit to you although your score is low, or decline your request for credit although your score is high.

Fallacy: A poor score will haunt me forever.

Fact: Just the opposite is true. A score is a "snapshot" of your risk at a particular point in time. It changes as new information is added to your bank and credit bureau files. Scores change gradually as you change the way you handle credit. For example, past credit problems impact your score less as time passes. Lenders request a current score when you submit a credit application, so they have the most recent information available. Therefore by taking the time to improve your score, you can qualify for more favorable interest rates. See how improved scores can lead to savings.

Fallacy: Credit scoring is unfair to minorities.

Fact: Scoring considers only credit-related information. Factors like gender, race, nationality and marital status are not included. In fact, the Equal Credit Opportunity Act (ECOA) prohibits lenders from considering this type of information when issuing credit. Independent research has been done to make sure that credit scoring is not unfair to minorities or people with little credit history. Scoring has proven to be an accurate and consistent measure of repayment for all people who have some credit history. In other words, at a given score, non-minority and minority applicants are equally likely to pay as agreed.

Fallacy: Credit scoring infringes on my privacy.

Fact: Credit scoring evaluates the same information lenders already look at — the credit bureau report, credit application and/or your bank file. A score is simply a numeric summary of that information. Lenders using scoring sometimes ask for less information " fewer questions on the application form, for example.

Fallacy: My score will drop if I apply for new credit.

Fact: If it does, it probably will not drop much. If you apply for several credit cards within a short period of time, multiple requests for your credit report information (called "inquiries") will appear on your report. Looking for new credit can equate with higher risk, but most credit scores are not affected by multiple inquiries from auto or mortgage lenders within a short period of time. Typically, these are treated as a single inquiry and will have little impact on the credit score.

Tips for Improving Your Credit Score:

-

Payment History

- Pay your bills on time. Delinquent payments and collections can have a major negative impact on your score.

- If you have missed payments, get current and stay current. The longer you pay your bills on time, the better your score.

- Be aware that paying off a collection account will not remove it from your credit report. It will stay on your report for seven years.

- If you are having trouble making ends meet, contact your creditors or see a legitimate credit counselor. This will not improve your score immediately, but if you can begin to manage your credit and pay on time, your score will get better over time.

-

Amounts Owed

- Keep balances low on credit cards and other "revolving credit". High outstanding debt can affect a score.

- Pay off debt rather than moving it around. The most effective way to improve your score in this area is by paying down your revolving credit. In fact, owing the same amount but having fewer open accounts may lower your score.

- Do not close unused credit cards as a short-term strategy to raise your score.

- Do not open a number of new credit cards that you do not need, just to increase your available credit. This approach could backfire and actually lower your score.

-

Length of Credit History

- If you have been managing credit for a short time, do not open a lot of new accounts too rapidly. New accounts will lower your average account age, which will have a larger effect on your score if you do not have a lot of other credit information. Also, rapid account buildup can look risky if you are a new credit user.

-

New Credit

- Do your rate shopping for a given loan within a focused period of time. Credit scores distinguish between a search for a single loan and a search for many new credit lines, in part by the length of time over which inquiries occur.

- Re-establish your credit history if you have had problems. Opening new accounts responsibly and paying them off on time will raise your score in the long term.

- Note that it is OK to request and check your own credit report. This will not affect your score, as long as you order your credit report directly from the credit reporting agency or through an organization authorized to provide credit reports to consumers.

-

Types of Credit Use

- Apply for and open new credit accounts only as needed. Do not open accounts just to have a better credit mix — it probably will not raise your score.

- Have credit cards — but manage them responsibly. In general, having credit cards and installment loans (and paying timely payments) will raise your score. Someone with no credit cards, for example, tends to be higher risk than someone who has managed credit cards responsibly.

- Note that closing an account does not make it go away. A closed account will still show up on your credit report, and may be considered by the score.